*This is an update for Toronto as a whole and things can look very different between different areas and home types. If you would like to dig deeper into the numbers that matter more to you, please book a call with me here.

Key Takeaways:

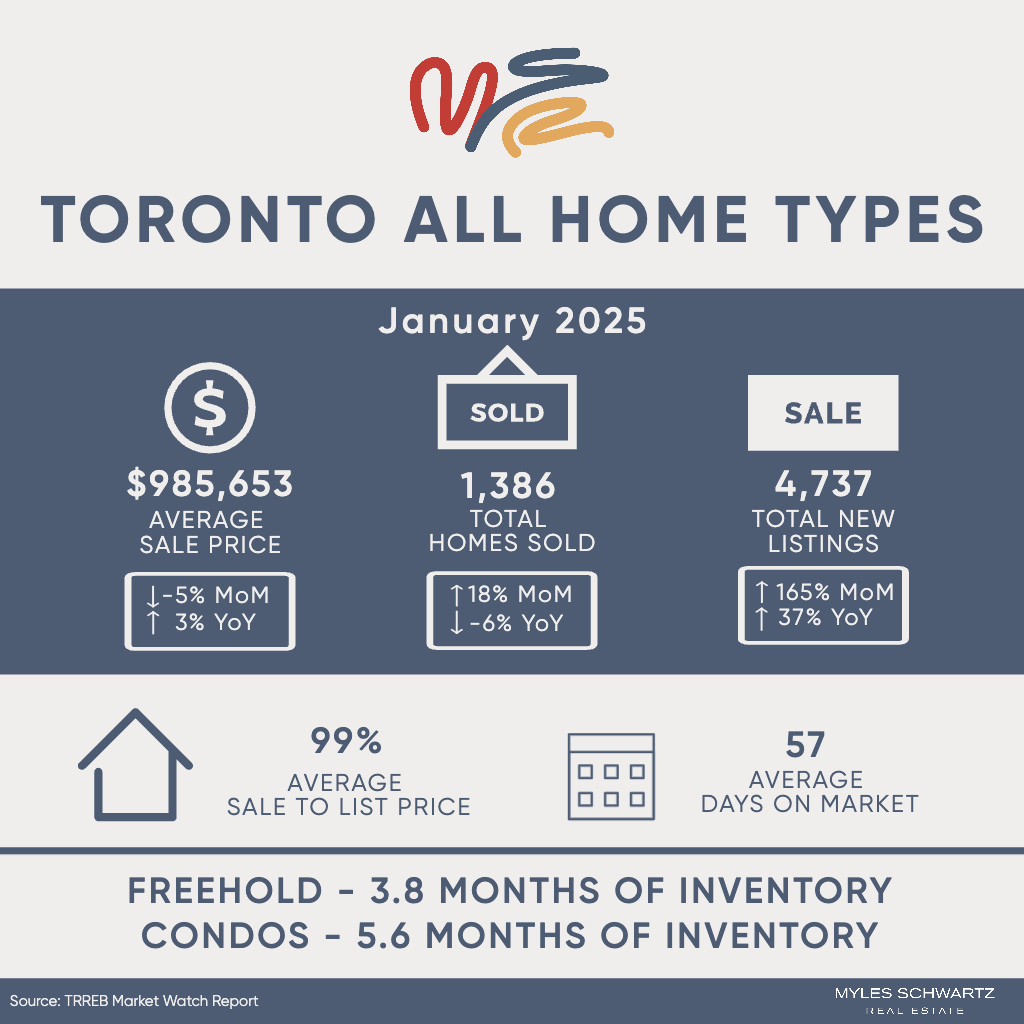

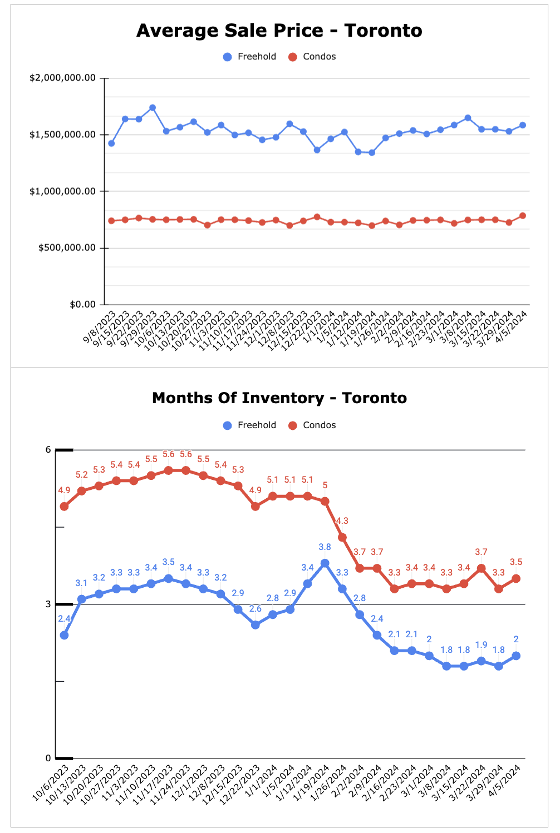

Prices are up year over year and down month over month.

Sales are down year over year.

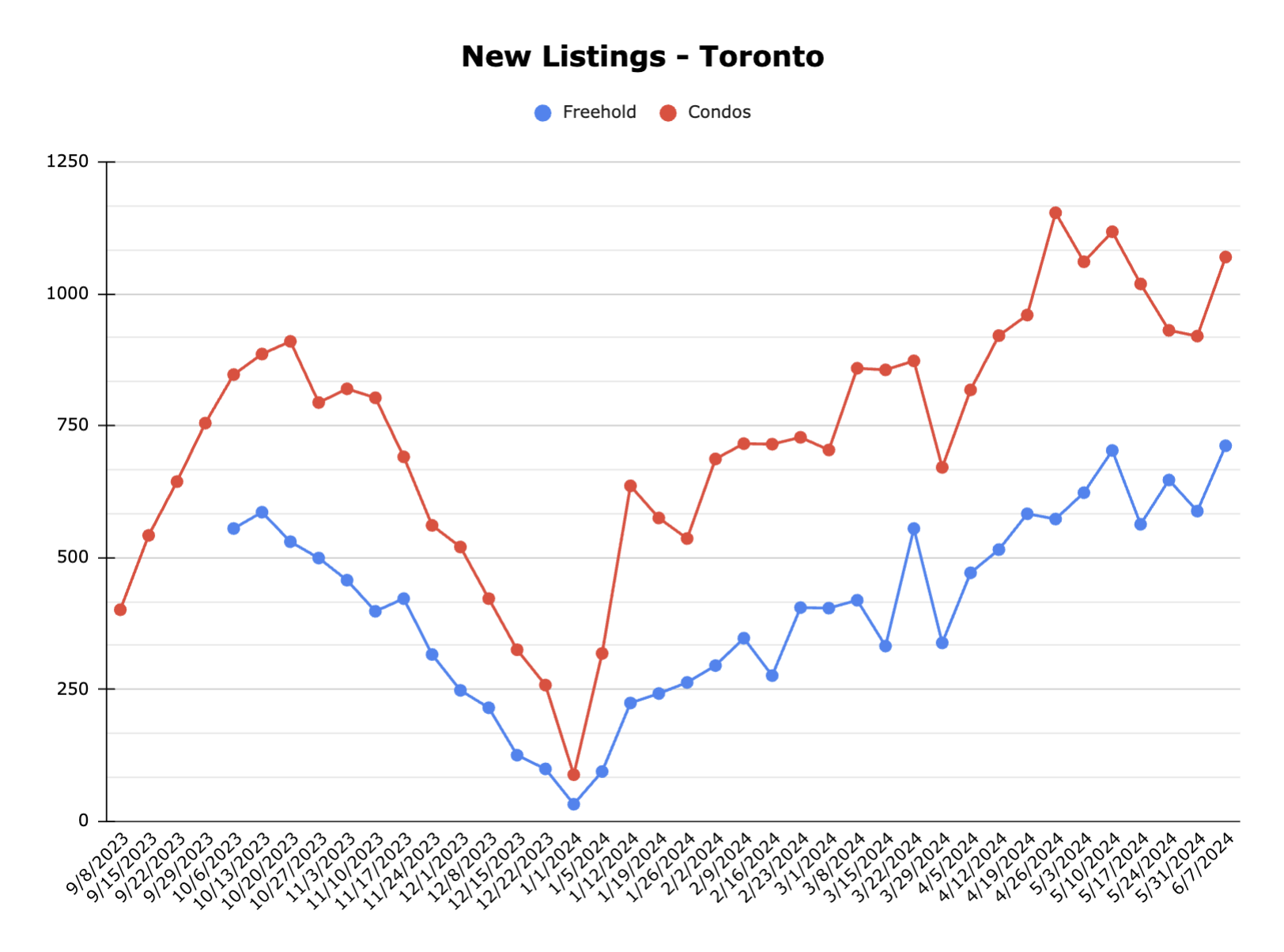

New Listings are way up year over year.

Majority of homes available for sale are condos and thats what is hurting most right now.

Freehold homes still have a lot of demand, especially in the 1m-1.5m rage.

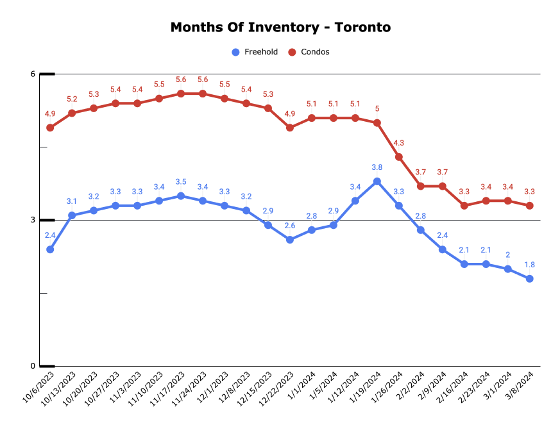

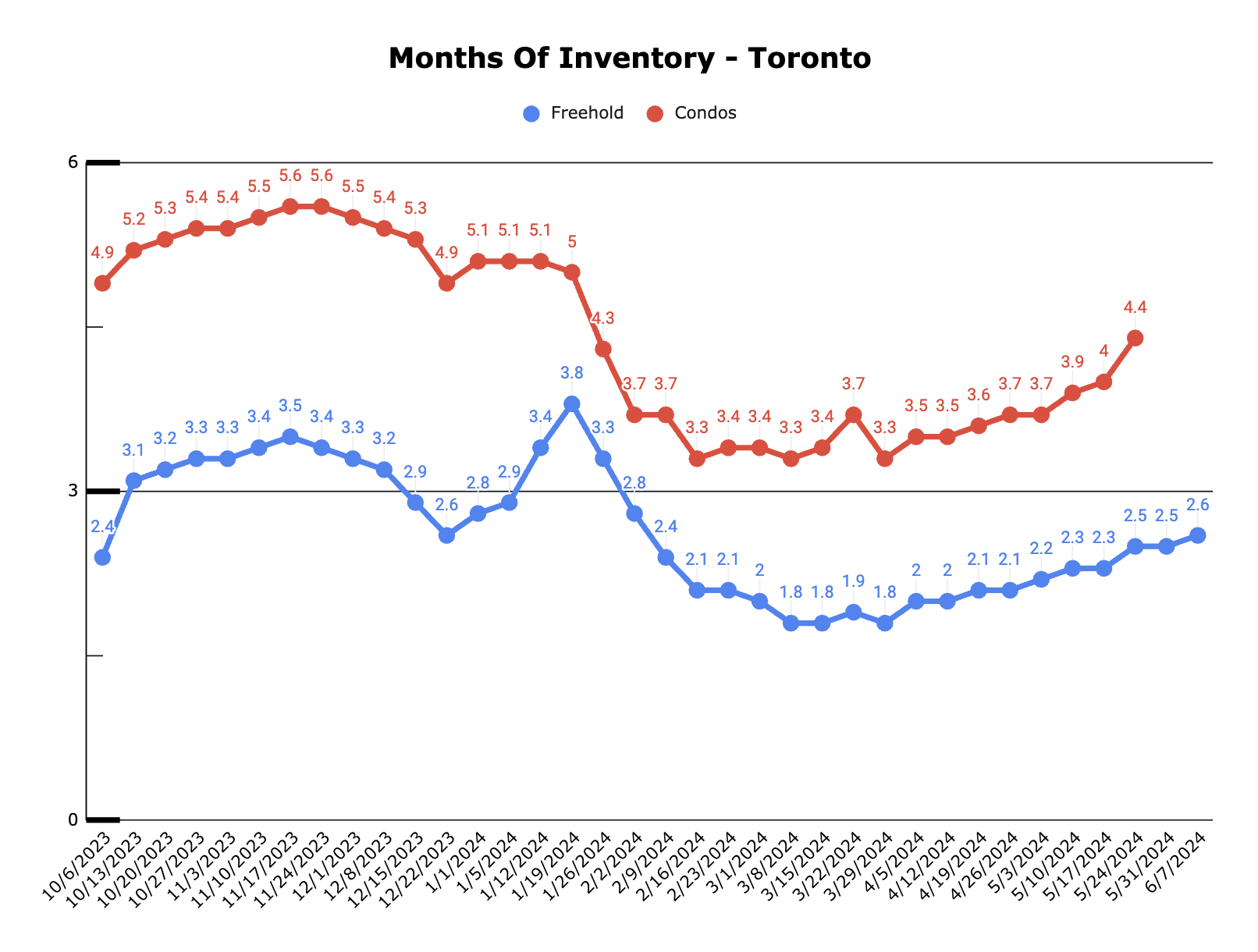

Looking at numbers after the first couple weeks of February, Toronto Freehold homes are in a Balance Market at 3.8 Months Of Inventory and Toronto Condos are on the cusp of a Buyers Market at 5.6 Months Of Inventory.

*This is an update for Toronto as a whole and things can look very different between different areas and home types. If you would like to dig deeper into the numbers that matter more to you, please book a call with me here.

Key Takeaways:

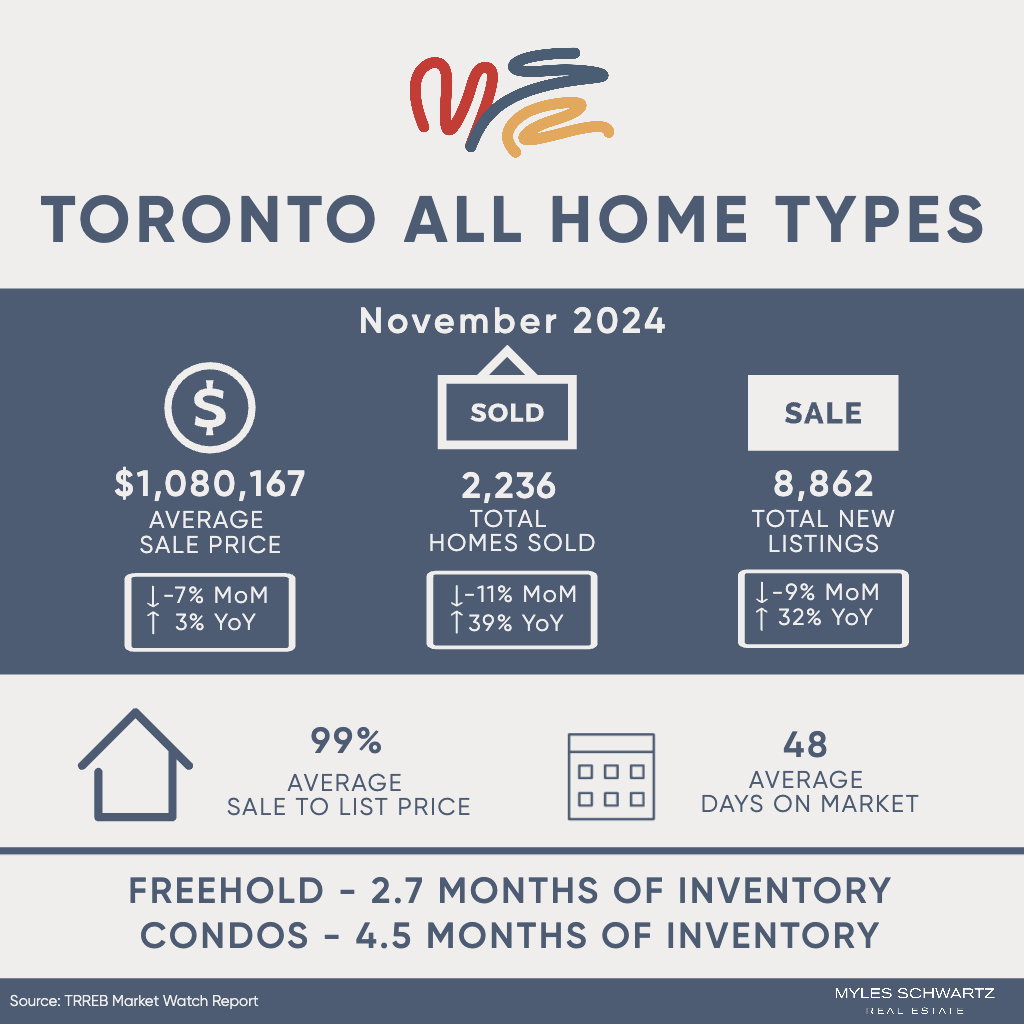

Prices are down YoY and down MoM.

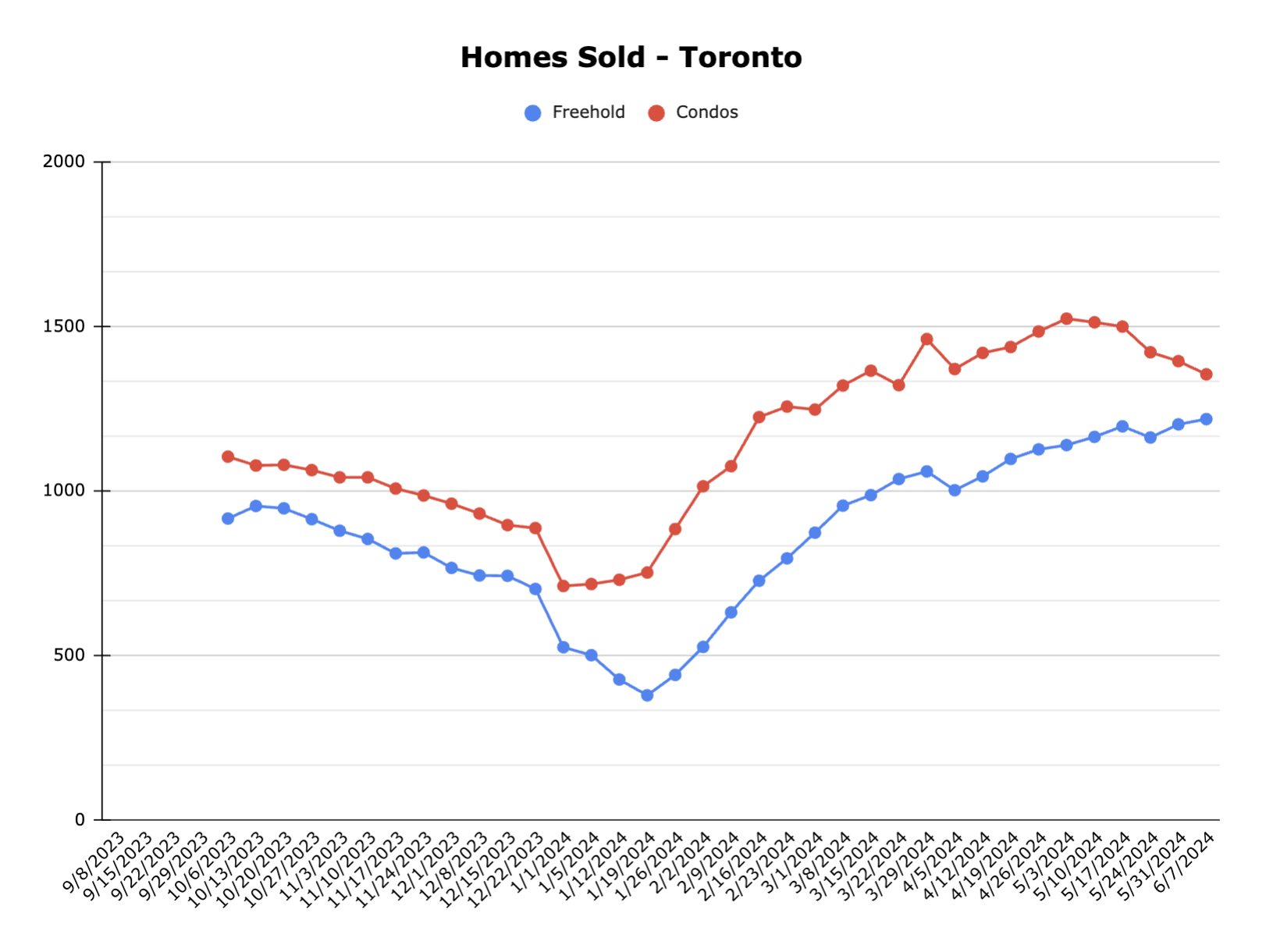

Sales are up down and down MoM.

New Listings are up YoY and down MoM.

Months of inventory has been steadily climbing over the past few weeks in all categories.

Looking at numbers after the first couple weeks of January, Toronto Freehold homes are in a Balance Market at 2.7 Months Of Inventory and Toronto Condos are up in a Buyers Market at 4.5 Months Of Inventory.

*This is an update for Toronto as a whole and things can look very different between different areas and home types. If you would like to dig deeper into the numbers that matter more to you, please book a call with me here.

Key Takeaways:

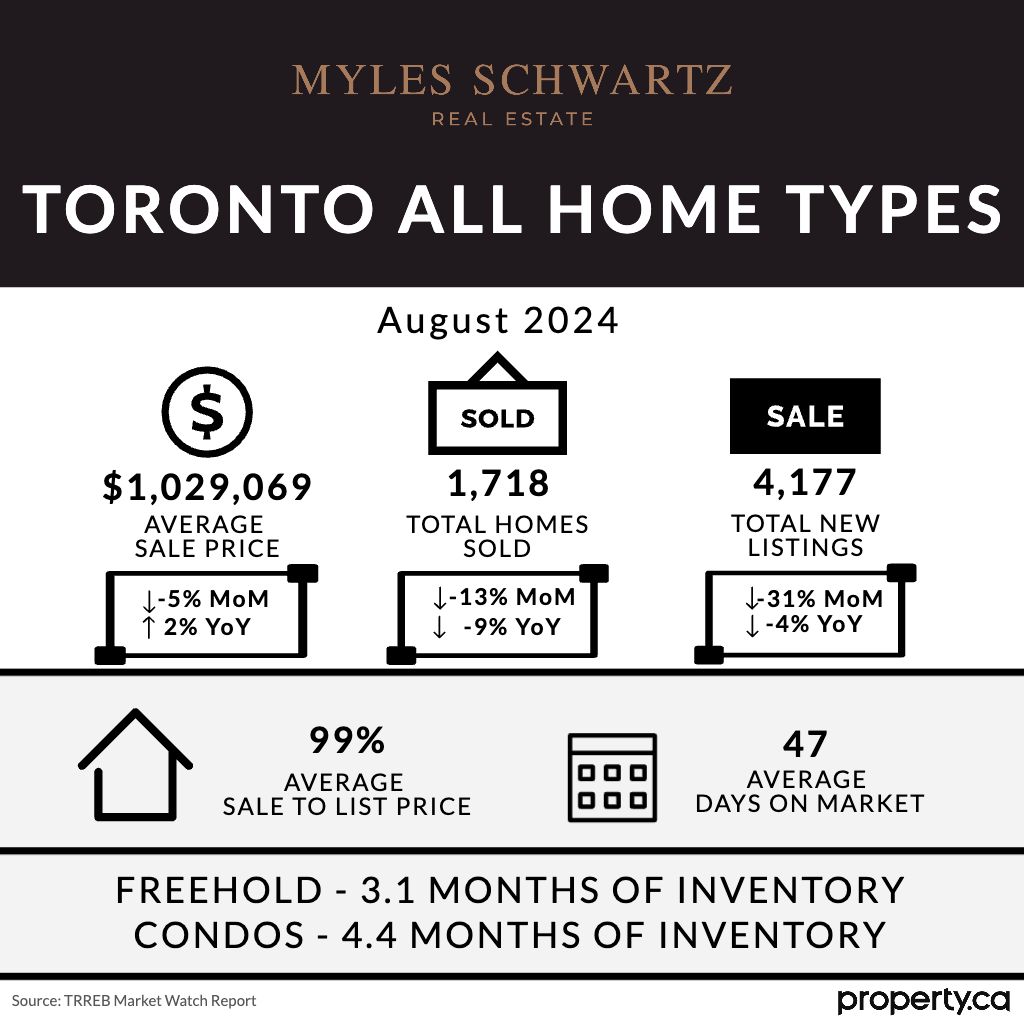

Prices are up YoY and down MoM.

Sales are up YoY and down MoM.

New Listings are up YoY and down MoM.

The Bank of Canada reduced their rate another .5%.

There is a ton of anticipation for the new year as interest rates are finally more affordable and the government has implemented new policies that came into effect December 15th to improve affordability for homes under $1.5M.

We are still dealing with two very different markets between Freehold and Condos as Freehold is still moving while Condos remaining more stagnant.

Looking at numbers after the first week of September, Toronto Freehold homes are in a Balance Market at 2.7 Months Of Inventory and Toronto Condos are up in a Buyers Market at 4.5 Months Of Inventory.

*This is an update for Toronto as a whole and things can look very different between different areas and home types. If you would like to dig deeper into the numbers that matter more to you, please book a call with me here.

Key Takeaways:

Prices are up.

Sales are up.

New Listings are up.

The market is finally starting to feel the affects of the rate cuts as buyer activity picks up.

Around now, sellers with stale listings will start to take them down with the intention of re-listing next year when the market picks up more.

New listings that come to market from now until the end of the year are likely being listed by desperate sellers that need to sell creating opportunity for buyers.

Looking at numbers after the first week of September, Toronto Freehold homes are in a Balance Market at 2.8 Months Of Inventory and Toronto Condos are up in a Buyers Market at 5.1 Months Of Inventory.

*This is an update for Toronto as a whole and things can look very different between different areas and home types. If you would like to dig deeper into the numbers that matter more to you, please book a call with me here.

Key Takeaways:

Prices are down.

Sales are up.

New Listings are way up.

Days on market are down.

The next rate announcement by the Bank Of Canada is October 23rd and it is expected to be another cut.

Looking at numbers after the first week of September, Toronto Freehold homes are in a Balance Market at 3.4 Months Of Inventory and Toronto Condos are up in a Buyers Market at 6.1 Months Of Inventory.

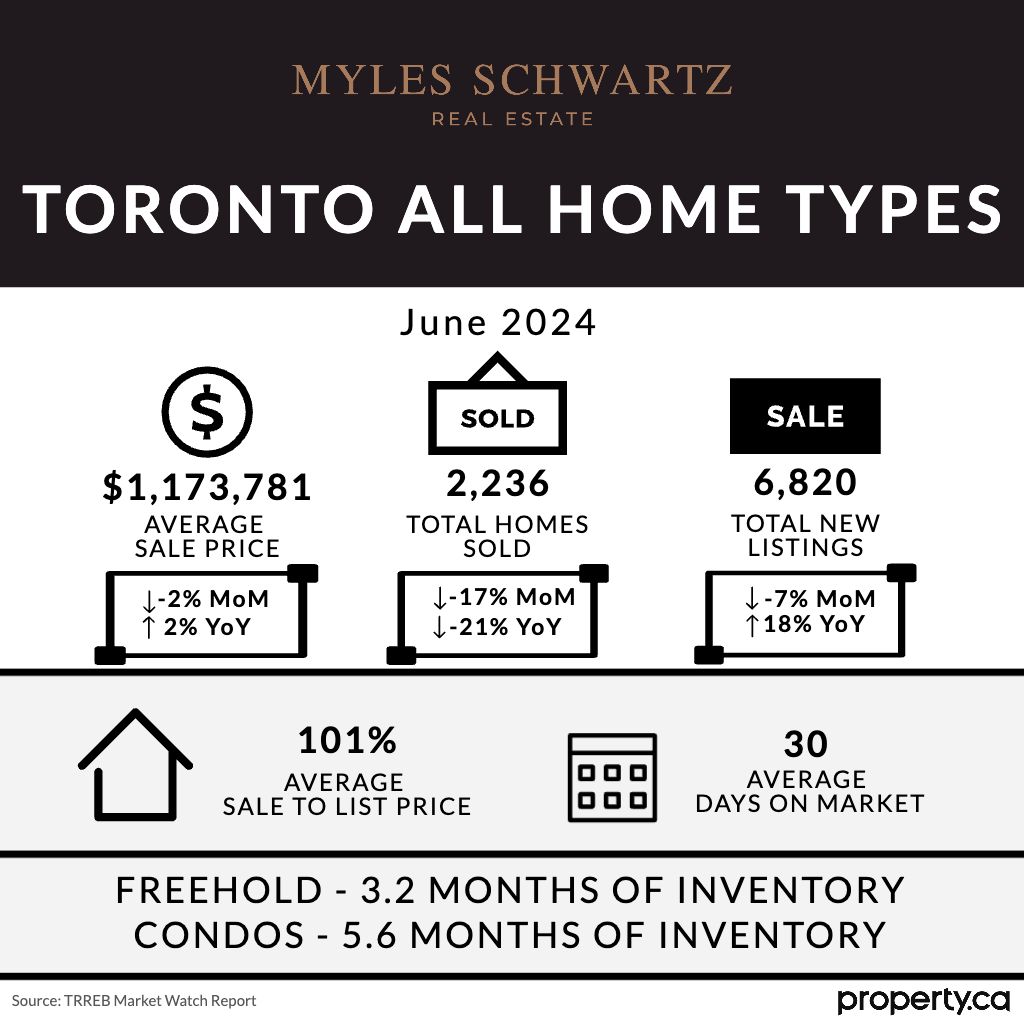

*This is an update for Toronto as a whole and things can look very different between different areas and home types. If you would like to dig deeper into the numbers that matter more to you, please book a call with me here.

Key Takeaways:

Prices are down.

Sales are down.

New Listings were down.

Days on market are up.

September should see an increase in activity for both buyers and sellers.

New listings are already way up week over week since labour day weekend.

The Bank Of Canada cut their overnight rate again and it looks like they are likely to cut at each announcement for the remainder of the year (October 23rd and December 11th are the next two rate announcements)

Looking at numbers after the first week of September, Toronto Freehold homes are in a Balance Market at 4.1 Months Of Inventory and Toronto Condos are up in a Buyers Market at 6.3 Months Of Inventory.

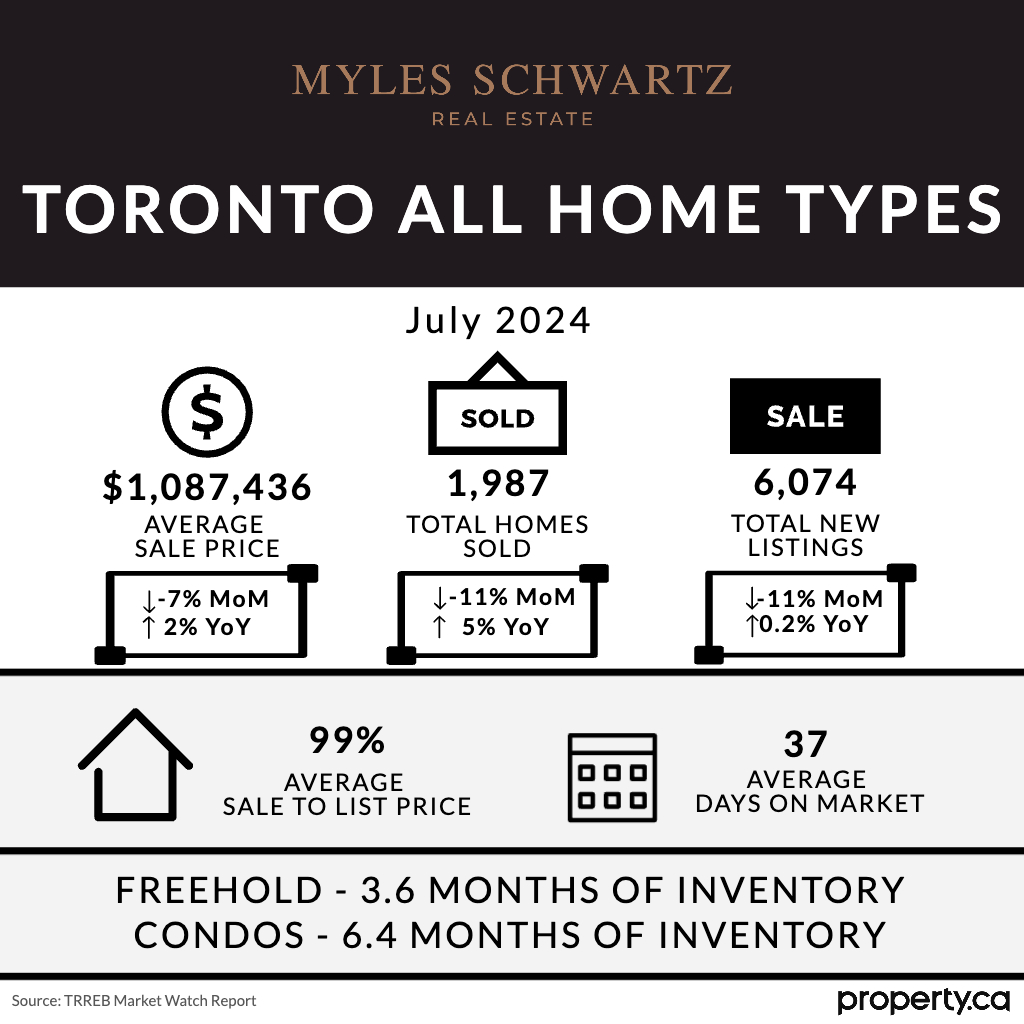

*This is an update for Toronto as a whole and things can look very different between different areas and home types. If you would like to dig deeper into the numbers that matter more to you, please book a call with me here.

Key Takeaways:

Prices are down.

Sales are down.

New Listings are down.

Days on market are up.

August is usually the slowest month of the year so expect this trend to continue.

The next Bank Of Canada Rate announcement is September 4th.

Looking at numbers after the first week of July, Toronto Freehold homes are in a Balance Market at 3.6 Months Of Inventory and Toronto Condos are up in a Buyers Market at 6.4 Months Of Inventory.

*This an update for Toronto as a whole and things can look very different between different areas and home types. If you would like to dig deeper into the numbers that matter more to you, please book a call with me here.

Key Takeaways:

Prices have come down a little bit.

There are lots of options for buyers right now.

If things continue moving as they are now, prices will come down more.

The Bank of Canada interest rate announcement has had no effect on the market so far.

The summer is a slow time for real estate and I expect things to be slow until at least September.

Looking at numbers after the first week of July, Toronto Freehold homes are now up in a Balance Market at 3.2 Months Of Inventory and Toronto Condos are up in a Buyers Market at 5.6 Months Of Inventory.

The amount of homes available for sale continued to go up.

Prices remained relatively flat.

Simply put, Detached and Semi-Detached freehold homes are in a sellers market and condos are leaning into a buyers market.

Sales activity was very slow as many buyers were “waiting to see whats going to happen with interest rates”

The Bank Of Canada lowered interest rates .25% which will save variable rate holders about $10-15 less per $100,000 of their mortgage. (June will be a good test to see how people actually react to this)

Running numbers after the first week of June, Toronto Freehold homes are up at 2.5 Months Of Inventory (Sellers Market) and Toronto Condos are up at 4.9 Months Of Inventory (Balanced Market).

Data below.

*I intentionally like to keep these reports short and straightforward. If you have questions about any specific aspect of the market or want me to expand on the data shared, please reach out.

Average sale price in April was up 6% month over month and 3% year over year.

Another big jump in sales activity as April saw a 12% increase in homes sold month over month but still 6% lower than this time last year.

Inventory is continuing to pile on with a 35% increase in new homes month over month and 52% year over year.

Out of all these listings, the vast majority are coming from condos.

Running numbers after the first week of April, Toronto Freehold homes are at 2.2 Months Of Inventory (Sellers Market) and Toronto Condos are at 3.7 Months Of Inventory (Balanced Market).

Data below.

*I intentionally like to keep these reports short and straightforward. If you have questions about any specific aspect of the market or want me to expand on the data shared, please reach out.

Average sale price in March was relatively flat with a slight uptick month over month and year over year.

Another big jump in sales activity as March saw a 17% increase in homes sold month over month but still 9% lower than this time last year.

Inventory is continuing to roll on to the market with a 42% increase in new homes month over month and 14% year over year.

This time last year saw a surge in activity with new found activity in buyers as there was false confidence that rates would be coming down and the market took off. The fact that we have 9% less sales and 14% more homes to sell tells me we are just in a healthier balance right now.

March saw an Easter weekend for the first time in a long time which is typically a slow few days for real estate and I imagine that was factored in to seeing a decline in number of sales year over year. I anticipate April is likely to be much more active for both buyers and sellers across the board.

Running numbers after the first week of April, Toronto Freehold homes are at 2 Months Of Inventory (Sellers Market) and Toronto Condos are at 3.5 Months Of Inventory (Balanced Market).

Data below.

*I intentionally like to keep these reports short and straightforward. If you have questions about any specific aspect of the market or want me to expand on the data shared, please reach out.

Average sale price in February was up 11% month over month and unchanged year over year. This is largely being effected by the Freehold market.

February sees continued activity with another significant jump in buyer activity bith month over month and year over year.

More inventory has also been hitting the market however it hasnt been enough to keep up with demand in the Freehold sector.

The continuing trend of increased buyer activity in the Freehold market is causing the spike n average sale price however condos are remaining flat with no price dips or growth for now. If you are looking for deals, consider them gone from the freehold sector but there are still some potential deals lying around for condos if you know where to find them.

Running numbers after the first week of March, Toronto Freehold homes are down to 1.8 Months Of Inventory (Sellers Market) and Toronto Condos are down to 3.3 Months Of Inventory (Balanced Market).

Data below.

*I intentionally like to keep these reports short and straightforward. If you have questions about any specific aspect of the market or want me to expand on the data shared, please reach out.

This website may only be used by consumers that have a bona fide interest in the purchase, sale, or lease of real estate of the type being offered via the website.

The data relating to real estate on this website comes in part from the MLS® Reciprocity program of the PropTx MLS®. The data is deemed reliable but is not guaranteed to be accurate.

-560-wide.jpeg)

-560-wide.jpeg)